Startup News Roundup - Week of May 5-10, 2026 The Week AI Infrastructure Became the World's Most Actively Funded Asset Class

Editorial Team

Last week, five deals told you more about the current state of the global startup market than any single article can convey. Taken together, they describe a market that has moved past the question of whether AI is transformative and arrived at the far more commercially interesting question of which layer of the AI stack captures the most durable value. The answer the capital is giving is infrastructure, and it is giving it loudly.

Here is everything that happened.

The Infrastructure Story of the Week: RadixArk's $100 Million Seed

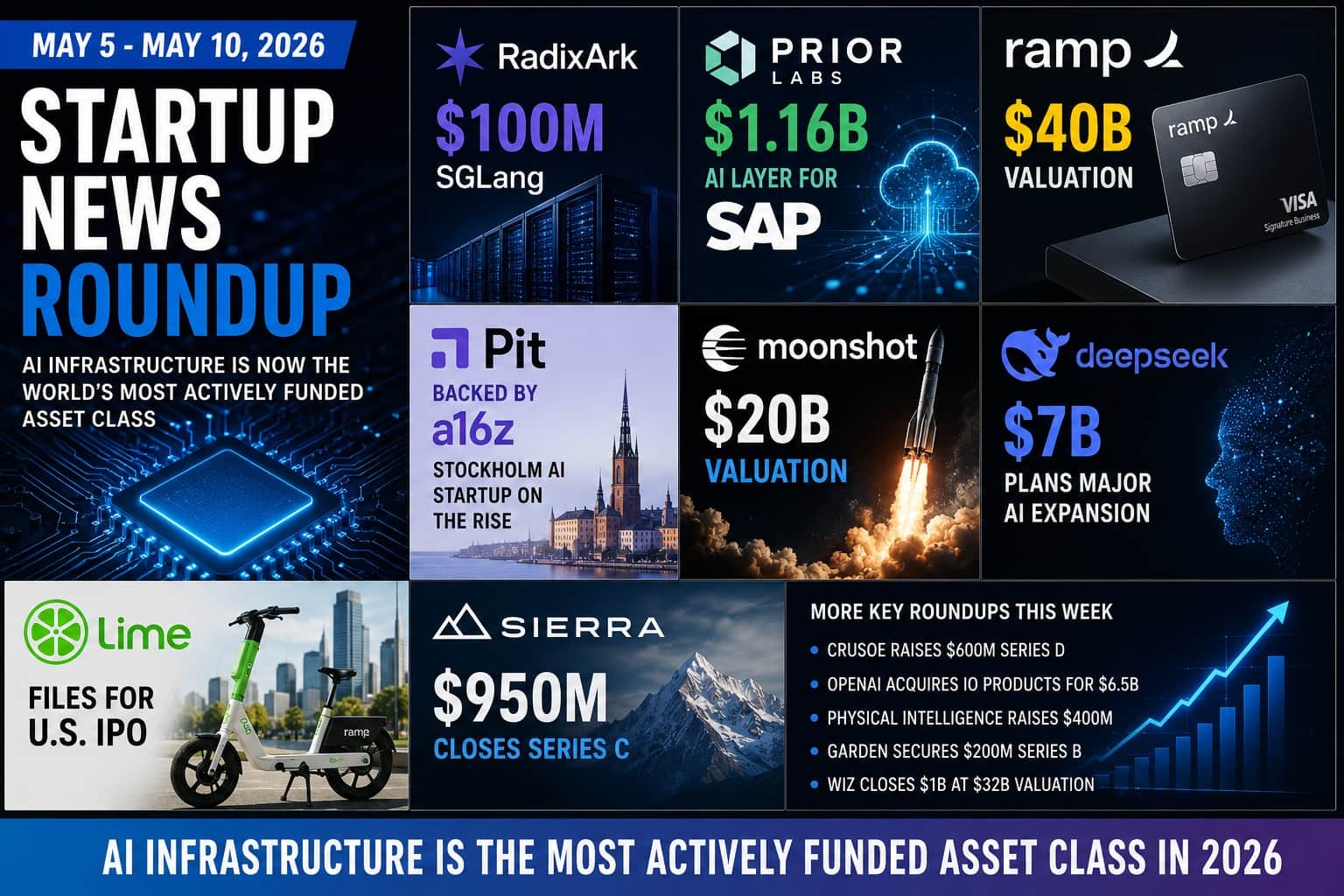

Open‑source AI tools are becoming commercial companies at an accelerating pace, and the week's clearest example of that trend was RadixArk, which launched on May 5 with $100 million in seed funding at a $400 million valuation led by Accel and Spark Capital.

The company was built by Ying Sheng, a former xAI engineer, and Banghua Zhu, a former Nvidia researcher, to commercialize SGLang, the open‑source inference engine they created in 2023 that is already processing trillions of tokens daily for Google, Microsoft, xAI, Oracle, and LinkedIn. The angel investor list, which includes the CEO of Intel, the CEO of Broadcom, John Schulman from OpenAI, and Soumith Chintala, the creator of PyTorch, confirms that the inference engineering community considers SGLang genuinely important infrastructure.

The business model mirrors what Databricks did with Spark: keep the open‑source project free and improve it with the community, charge for managed hosting and enterprise support. A parallel company, vLLM, another UC Berkeley‑incubated inference project, is separately raising approximately $160 million from Andreessen Horowitz at roughly a $1 billion valuation. The simultaneous commercialization of two competing open‑source inference engines confirms that the market for inference optimization infrastructure is real, large, and willing to pay at scale.

Why it matters for the broader ecosystem: Every time a popular open‑source AI project raises institutional capital at hundreds of millions in valuation, it signals that the layer between foundation models and production deployments is becoming a commercial priority rather than a charity maintained by academic researchers. Teams building on SGLang or vLLM now have commercially supported infrastructure they can rely on without rebuilding inference stacks from scratch.

Europe Had Its Biggest AI Funding Week Ever

Two European AI stories this week represent the largest private AI investment in European history and one of the most significant new enterprise AI companies to emerge from the continent.

Prior Labs, the Munich‑based startup building tabular foundation models for enterprise structured data, received a $1.16 billion investment from SAP, making it Europe's best‑funded private AI lab. Co‑founded by researchers Noah Hollmann and Samuel Müller, Prior Labs is building AI specifically for the 90 percent of enterprise data that exists as structured tables rather than text. SAP's bet is that the AI layer for enterprise business intelligence needs to be built for tabular data natively, not translated through text‑based models that lose most of the relational structure. The $1.16 billion, the largest single AI investment in European startup history, reflects SAP's conviction that this technical approach will define enterprise AI for the next decade.

Pit, the Stockholm startup founded by Voi and Klarna alumni, raised a $16 million seed led by a16z, with Lakestar and angels from OpenAI, Anthropic, Google, Deel, and Revolut participating. The company builds custom AI‑native enterprise software in days rather than months, replacing the spreadsheets, email threads, and rigid SaaS tools that currently run most large‑company operations. Customers at Voi, Tre, Stena Recycling, and Kry are reporting 85 percent reductions in campaign execution time and 10,000‑plus hours saved annually. Fredrik Hjelm, Voi's CEO and a Pit co‑founder, described the a16z relationship as built over years, not manufactured for a fundraise.

Stockholm's emergence as Europe's most active AI startup hub is no longer a developing story. It is a documented pattern. The city that produced Voi, Klarna, iZettle, Spotify, and King is now producing AI‑native enterprise companies that attract US tier‑one venture capital at seed stage.

The US Fintech Story: Ramp Targets $40 Billion, Six Months After $32 Billion

Ramp, the corporate spend management platform that crossed $1 billion in annualized revenue last year, is in advanced talks to raise $750 million at a pre‑money valuation exceeding $40 billion, The Wall Street Journal reported on May 7. The round would be co‑led by GIC and Iconiq Capital, both returning investors, and would bring Ramp's total equity raised to approximately $3 billion.

The company is reportedly in talks to raise another $750 million at a pre‑money valuation of more than $40 billion. It last raised in November at $32 billion.

The context that makes this trajectory meaningful rather than speculative: Brex, Ramp's primary independent competitor, was acquired by Capital One in January 2026 for $5.15 billion, a fraction of its peak private valuation. Ramp has now monopolized the independent corporate spend management category, serving 50,000‑plus companies with an estimated 98 percent of its total addressable market remaining. The $40 billion at $1 billion ARR implies a 40x revenue multiple, which is aggressive and also consistent with a company that has grown revenue 100 percent year‑over‑year, generated positive cash flow, and has no significant independent competitor remaining.

Ramp has told investors it plans to be IPO‑ready by the end of 2026. The prediction market Kalshi assigns approximately 30 percent probability to a Ramp IPO before May 2027. Whether the public listing comes this year or next, the company's status as the dominant private fintech in its category, following Brex's exit, makes it one of the most anticipated listings in the pipeline.

The China AI Funding Race Intensified

Two major China AI developments this week confirm that the frontier model market is a genuinely global competition with the capital flows to match.

Moonshot AI completed a $2 billion raise at a $20 billion valuation, led by Meituan's Long‑Z Investments with Tsinghua Capital, China Mobile, and CPE Yuanfeng. The company hit $100 million ARR in March and $200 million ARR in April, a doubling in approximately four weeks. Its Kimi K2.6 model is currently the second most‑used LLM on OpenRouter, with 47 percent American users, confirming that Chinese open‑weight models are winning on technical quality in markets outside China. Total capital raised by Moonshot in the past six months has reached $3.9 billion.

DeepSeek, which has operated self‑funded since founding through High‑Flyer, founder Liang Wenfeng's quantitative hedge fund, is reportedly seeking to raise up to 50 billion yuan, approximately $7.35 billion, in its first external round. The Information's reporting cites two people familiar with the discussions who describe the raise as accelerating DeepSeek's plans to generate revenue and increase model release frequency. China's National Integrated Circuit Industry Investment Fund is in talks as a potential lead external investor, alongside Tencent, which is reportedly considering a $3 to $4 billion participation.

The pattern across both Moonshot and DeepSeek is the same: Chinese AI labs that demonstrated technical quality through open‑weight releases are now converting that technical credibility into institutional capital and commercial revenue, following a trajectory similar to what OpenAI and Anthropic executed in 2023 and 2024.

The IPO That Cannot Wait: Lime Files Its S‑1

The week's most consequential public market development was not a funding round but an IPO filing. Lime, the Uber‑backed electric scooter and e‑bike operator, filed its S‑1 with the SEC on May 7 under its corporate name Neutron Holdings, with Goldman Sachs and JPMorgan leading the syndicate and the ticker "LIME" reserved on Nasdaq.

After years of hints and preparation, the Uber‑backed electric bike and scooter rental startup Lime has filed for an initial public offering. The company, which is incorporated as Neutron Holdings, Inc., has eyed the public markets for at least five years.

Lime posted a 29% rise in revenue to $886.7 million and a loss of $59.3 million in 2025.

The disclosure that changes the IPO calculus is a going‑concern warning. Lime reported around $1 billion in current liabilities in the filing. Roughly $846 million of that is due 12 months from now. About $675.8 million is due by the end of 2026. The company wrote that it does not have "sufficient liquidity" to pay that. With $261 million in cash on March 31, the IPO is not optional. It is the mechanism for resolving a debt maturity timeline that the company's existing cash position cannot cover.

Renaissance Capital estimates the offering could raise approximately $250 million. Whether that is sufficient to service $846 million in near‑term obligations depends on additional financing arrangements that the S‑1 does not yet specify. The business itself, 3.8 million monthly active users, 325,000 vehicles, $7.47 revenue per vehicle per day, is operationally sound. The debt structure is the constraint, and the roadshow will need to make that case persuasively.

The Week's Signal for Founders and Investors

The pattern across every major deal from May 5 through May 10 is the same one that has defined 2026 since January: the highest valuations and the largest checks are going to companies that own a critical layer of the AI stack, serve it as infrastructure rather than a feature, and have demonstrated that other companies cannot easily build without them.

RadixArk is infrastructure. Prior Labs is infrastructure. Ramp is financial infrastructure. Pit, at its best, is operational infrastructure. Sierra is the customer experience infrastructure layer. Moonshot is model infrastructure for an ecosystem of applications that will be built on top of it.

The companies raising at nine and ten figure valuations are not, with rare exceptions, the companies with the most impressive product demos. They are the companies that other companies are paying for as operational necessities rather than discretionary additions. In the AI era, infrastructure is not a sector. It is the strategy.

Stay informed

Startup news in your inbox

Get important funding rounds, founder stories, and startup updates.

No spam - only important startup updates.