Startup News Today May 5, 2026 | Sierra $950M, Parallel $2B, Forbes AI 50, DeepSeek V4 Daily Roundup

Editorial Team

It is Tuesday, May 5, 2026. Here is everything you need to know from the startup and technology world before you open your second browser tab.

The theme this week is infrastructure. Not in the abstract sense that AI commentators invoke when they want to sound serious, but in the literal, specific, commercially consequential sense: the pipes, APIs, inference layers, legal rails, and customer‑facing agents that sit between foundation models and the people who use them. Every major deal this week either builds that infrastructure or depends on it. The startups winning the largest rounds are the ones that have quietly become necessary for everyone else.

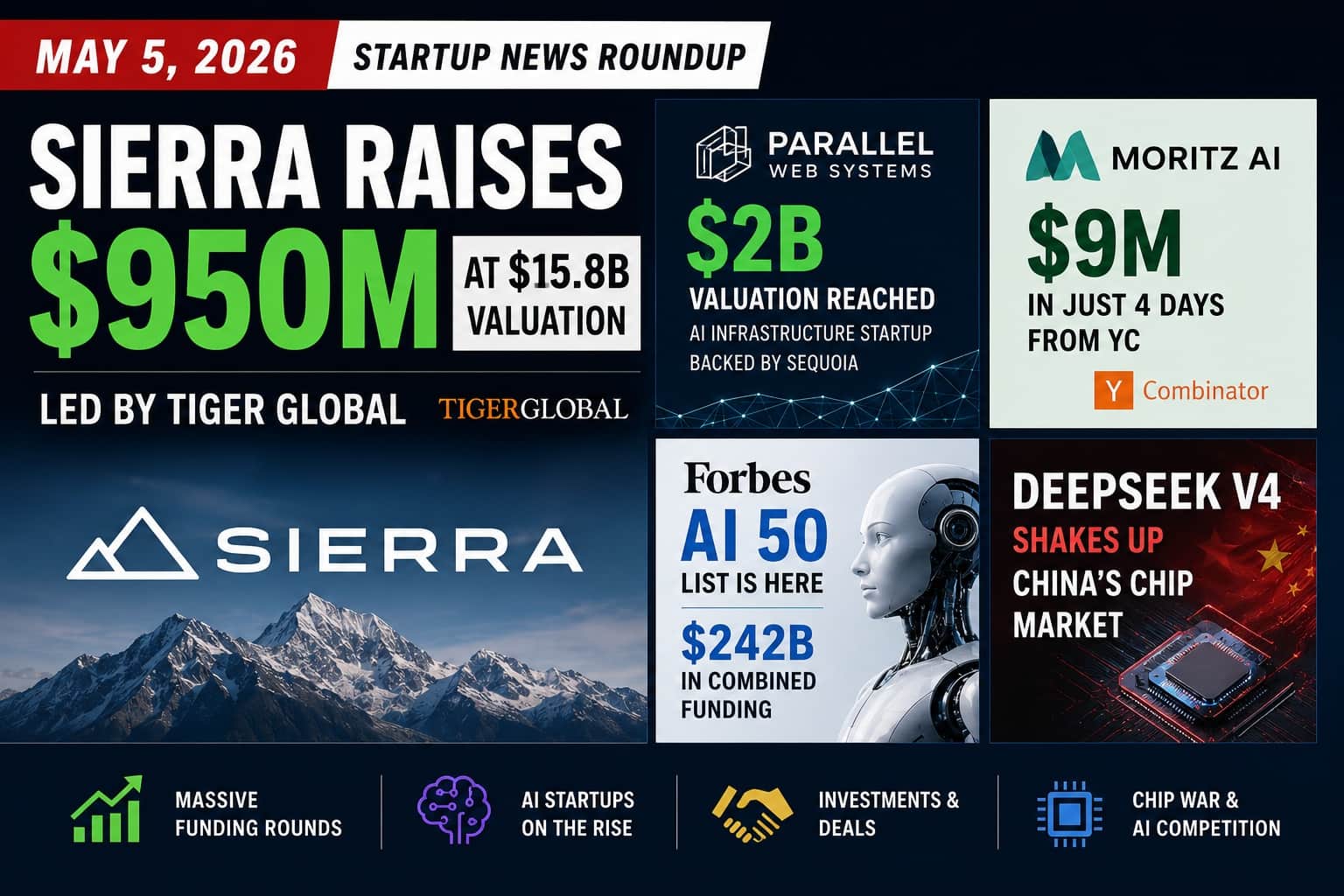

Sierra Raises $950 Million at $15.8 Billion. Bret Taylor Says the Customer Service Category Is His.

The biggest deal of the week did not come from an infrastructure company. It came from the company that has quietly built the largest commercial AI customer service platform on earth.

Sierra, the San Francisco company co‑founded by OpenAI Chairman and former Salesforce co‑CEO Bret Taylor and former Google executive Clay Bavor, raised $950 million in a Series E led by Tiger Global and Google's GV. Benchmark, Sequoia, Greenoaks, and other existing investors also participated. The post‑money valuation is $15.8 billion, making Sierra one of the most valuable private AI companies in the world outside of OpenAI, Anthropic, and xAI.

The commercial facts behind that valuation are specific and verifiable. Sierra's customers include Prudential, Cigna, Blue Cross Blue Shield, and Rocket Mortgage. One in three of the world's largest banks now uses its platform. Taylor told CNBC that Sierra is multiples larger than its next biggest competitor in the customer service agent category.

Peter Fenton, general partner at Benchmark and one of Sierra's first investors, said in an interview: "Sierra is by all measures the winner in the customer experience category, if measured by objective facts like scale of revenue and quality of customer base." He added that any company in traditional industries taking a watchful, waiting approach to AI is choosing a path to extinction.

The $950 million is Taylor's insurance policy on category leadership. "There's just a lot of competition," he said plainly. "We are multiples larger than the next biggest and are trying to invest aggressively so that we can continue to expand our lead."

Sierra has made three acquisitions in the past four weeks, including Paris‑based Fragment for European expansion, Japan's Opera Tech, and voice AI company Receptive AI. The pace of both organic growth and acquisitive expansion makes Sierra's trajectory one of the most compelling in enterprise AI this year.

Parallel Web Systems Hits $2 Billion in Five Months. Parag Agrawal Is Not Done.

Former Twitter CEO Parag Agrawal is having a second act that his first act could not have predicted.

Parallel Web Systems, the AI agent infrastructure company he co‑founded with Travers Nisbet in 2023, raised a $100 million Series B led by Sequoia Capital at a $2 billion valuation. Existing investors Kleiner Perkins, Index Ventures, Khosla Ventures, First Round Capital, Spark Capital, and Terrain Capital all returned. Sequoia partner Andrew Reed joined Parallel's board of directors as part of the deal.

This raise comes exactly five months after Parallel's $100 million Series A at a $740 million valuation, meaning the company's valuation has nearly tripled in five months and its total capital raised now stands at $230 million.

Parallel's product is not a consumer application or a B2B dashboard. It is a web search and research API infrastructure layer built specifically for AI agents. When an AI agent needs to retrieve real‑time information from the web, verify a fact, or research a topic during a multi‑step task, it uses services like Parallel's proprietary web index to do so accurately and at speed. Named customers include Clay, Harvey, Notion, Opendoor, Modal, Attio, and Rogo. More than 100,000 developers are active on the platform. Banks and hedge funds are customers, though none are named publicly.

Agrawal's description of the company's operating reality is refreshingly honest: "Every few weeks, we solve one bottleneck and hit another somewhere." The company plans to use the fresh capital to accelerate index growth, expand its enterprise customer base, and deepen the infrastructure layer that connects content and data owners with AI systems.

The Parallel story has a subtext worth acknowledging. After Elon Musk acquired Twitter in October 2022, Agrawal and other executives were terminated. A subsequent lawsuit over $128 million in unpaid severance was settled by Musk in October 2025 for undisclosed terms. The investor confidence that has taken Parallel from zero to $2 billion in three years is the cleanest available rebuttal to whatever that chapter cost him.

Moritz AI Raised $9 Million in Four Days. It Wants to Be an AI Law Firm, Not a Legal Tool.

The most interesting small deal of the week demonstrates something important: in 2026, the right founding credentials and the right YC batch can still convert into institutional capital in days rather than months.

Moritz AI, founded by Pamir Ehsas, who previously served as outside counsel to OpenAI, raised $9 million from Y Combinator, 20VC, and other investors in four days. The startup is building a flat‑fee AI law firm, positioning itself not as a software tool for existing legal workflows but as a replacement for the hourly billing model itself.

The founding story matters here. Ehsas's years as outside counsel to OpenAI gave him direct experience of what happens when AI‑native organizations need legal services and discover that traditional law firm pricing, structure, and speed are poorly matched to the pace of AI companies. Moritz AI is his answer to that structural mismatch, built for the clients he knows best.

The $9 million from YC and 20VC funds the team and platform build‑out. The four‑day close is the market's verdict on the founding team's credibility in the specific niche it is addressing.

Forbes AI 50 Is Out. Two Companies Have $242 Billion in Combined Funding and More Than $30 Billion in ARR.

Forbes published its annual AI 50 list this week, the publication's ranking of the most promising private AI companies globally. The 2026 list is anchored by OpenAI and Anthropic, which together have raised $242 billion in combined funding and are generating annualized revenue that exceeds $25 to $30 billion combined.

The 2026 list reflects themes that run through the entire week's news: specialization in coding agents and developer tools, robotics and embodied AI, open‑source model development, and creative tools that give non‑technical users production‑quality AI capabilities. Notable entries include Sierra, Cursor, Factory, Mistral, Rogo, Hightouch, and Featherless.ai, confirming that the AI 50 has moved from tracking research labs to tracking companies with measurable enterprise revenue.

The list also reflects the acquisition activity reshaping the market. Several companies that would have appeared on the AI 50 a year ago are now inside larger organizations, including ARI (acquired by Meta) and Fauna Robotics (acquired by Amazon).

DeepSeek V4 Just Became a Problem for Nvidia's China Strategy.

Outside the US funding news, the most consequential development of the week comes from China.

DeepSeek's V4 model launch is drawing significant attention from analysts who track China's AI chip ecosystem. The South China Morning Post reported that the model's technical capabilities and efficiency improvements are expected to boost demand for domestic Chinese AI chipmakers including Cambricon and Moore Threads, companies that make chips capable of running competitive models under the US export control regime that prevents China from buying Nvidia's highest‑performance GPUs.

The implication is commercially specific: if DeepSeek V4 performs well on domestic hardware, it reduces the commercial cost of US export controls on Nvidia for Chinese AI labs and enterprises. Beijing gains more room to build a domestically self‑sufficient AI ecosystem, and Nvidia loses potential future revenue from a market that continues to develop competitive AI systems regardless of chip access.

For Western founders and investors, the DeepSeek V4 development is a useful reminder that the AI race is not a two‑company competition between OpenAI and Anthropic. The open‑source competitive pressure is global, and the infrastructure assumptions underlying Western AI business models are being tested in real time.

OpenAI's Codex Giveaway Is Reaching 8,000 Developers.

OpenAI turned its sold‑out GPT‑5.5 launch event into a month‑long Codex access program for 8,000 developers, according to VentureBeat. The program gives developers hands‑on access to GPT‑5.5's agentic coding capabilities before a broader commercial rollout.

The commercial logic is clear: the 8,000 developers who experience Codex in a guided environment become the most credible evangelists for enterprise adoption. Jensen Huang's email to 10,000 Nvidia employees encouraging everyone to use Codex was the first data point that the product generates genuine enthusiasm among professional users. The 8,000‑developer program is OpenAI's attempt to replicate that enthusiasm across the developer ecosystem before GitHub Copilot and Cursor have time to respond at the same scale.

What to Watch the Rest of the Week

Three developments are worth monitoring as the week progresses.

The Fluidstack $1 billion round at an $18 billion valuation has been in advanced talks since Bloomberg reported it in mid‑April. No formal close has been announced. When it does close, it will be the largest single private AI infrastructure financing of the year.

Sam Altman's exploration of an Alphabet‑style structure for OpenAI, which would spin out robotics and consumer hardware units into independent subsidiaries with their own funding, is reportedly still in discussion. The structural change would allow OpenAI's core research and model business to maintain focus while the adjacent product categories raise capital independently.

The Forbes AI 50 coverage will surface throughout the week across enterprise technology media. Watch for enterprise buyers using the list as a procurement shortcut, as they have in previous years, which benefits smaller companies on the list disproportionately.

The Week's Macro Signal

The week of May 5, 2026 confirms a pattern that has been building since January: the AI market is not consolidating around a small number of vertically integrated giants. It is stratifying into a deep stack, with foundation model providers at the top, infrastructure and tooling layers in the middle, and vertical application companies at the base, each layer generating durable commercial value and attracting institutional capital.

Sierra is winning at the application layer. Parallel is winning at the infrastructure layer. Moritz is building a new professional services model on top of both. Every layer is attracting serious capital, and the companies that serve multiple layers simultaneously, like OpenAI's move into coding agents, Anthropic's legal plugins, and Meta's humanoid robot software licensing ambitions, are the ones creating the most complex competitive dynamics.

The race is not slowing down. The infrastructure is just getting more interesting.

Stay informed

Startup news in your inbox

Get important funding rounds, founder stories, and startup updates.

No spam - only important startup updates.